27 May 7 Smart Ways Defence Members Can Reduce Their Tax Bill

If you serve in the Australian Defence Force, you may be paying more tax than necessary. When it comes to military tax in Australia, missed deductions, complex allowances, and a unique pay structure can all add up. It can be easier than you think to leave money on the table.

ADF members across the Army, Navy, and Air Force face distinct financial circumstances. Frequent postings, time on deployment, and subsidised housing all shape your tax position. Yet many members stick to the basics when it comes to their tax return, and overlook legitimate ways to reduce their tax bill each year.

This guide walks through seven practical strategies to help ADF members reduce their tax bill. From claiming deductions to using property and super to your advantage, each approach may impact your taxable income depending on your circumstances.

Whether you are a corporal in Townsville or a lieutenant commander in Canberra, these defence tax tips apply across all ranks and services. Understanding your full tax position is one of the best ways to reduce your tax bill as an ADF member.

1. Claim Every Work-Related Tax Deduction

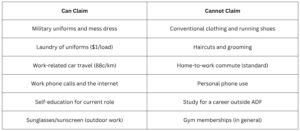

The quickest way to reduce your tax bill is to claim every deduction you are entitled to. Whether you are looking at Army tax deductions, Navy entitlements, or Air Force claims, ADF members can access a range of work-related expenses. Here is what the ATO says you can and cannot claim.

Uniforms, Protective Clothing, and Laundry

Your military uniforms are classified as compulsory work clothing by the ATO. You can claim the cost of purchasing, repairing, and maintaining them. This includes whites, blues, khakis, camouflage, mess dress, and regulation footwear.

Protective items like steel-capped boots, safety glasses, and sun-protective gear may also be claimed. These fall under the ATO’s protective clothing category and apply to a wide range of ADF roles.

Laundry costs are deductible, too. You can claim $1 per load for work-only washes, or $0.50 for mixed loads. If your total laundry claim is $150 or less, you do not need written evidence. You should still keep a record of how you calculated it.

One important detail: if you receive a uniform allowance, it must be declared as assessable income. You can then claim deductions for your actual uniform costs, which may offset that amount.

Car and Travel Expenses

Moving on to travel, you can claim car expenses for work-related trips. This includes travel between bases or to alternate work locations. The ATO’s cents-per-kilometre method allows you to claim 88 cents per kilometre, up to 5,000 km per year.

This rate covers fuel, registration, insurance, repairs, servicing, and depreciation in one calculation. You do not need individual receipts, but you should be able to show how you worked out your kilometres.

Alternatively, the logbook method may suit you. This requires a logbook for a continuous 12-week period to set your work-use ratio. It can result in a higher claim if you do a lot of work-related driving.

Keep in mind that your regular commute between home and base is generally not claimable. The exception is when you carry bulky equipment that cannot be stored at your workplace.

Phone, Internet, and Home Office Costs

If you use your personal phone or internet for work, you can claim the work-related portion. The ATO recommends keeping a four-week diary to set your usage ratio. You can then apply that ratio across the full year.

If you work from home on admin or coursework, you may also be able to claim. The ATO’s fixed rate method lets you claim a set rate per hour worked. It covers electricity, internet, phone, and stationery.

Computers and office furniture can be claimed separately. Items costing $300 or less qualify for an immediate deduction. Items over $300 are claimed through depreciation over their effective life.

If you use a device for both work and personal purposes, only the work portion is claimable. The ATO expects you to have records showing how you worked out the split.

Self-Education and Professional Subscriptions

Study that directly relates to your current ADF role may be deductible. This can include course fees, textbooks, travel to classes, and related equipment. The key is a clear link to your current duties.

You cannot claim courses designed to help you get a job outside the ADF. The distinction is about relevance to your current role. Courses funded through HECS-HELP are also not deductible.

Mess Fees and Union Dues

Mess subscriptions can be partially deductible. The work-related portion may be claimed, but the food, drink, and entertainment component is not deductible.

Union fees and professional association memberships are fully deductible. Tax agent fees for preparing your return can also be claimed.

What You Cannot Claim

It is worth knowing what falls outside the rules. Common expenses that ADF members cannot claim include:

- Conventional clothing and running shoes

- Haircuts and grooming, even if required by military regulations

- Gym memberships, unless your role requires above-standard fitness

- Personal phone usage

- Study for a career outside the ADF

- Your standard commute to and from base

ADF Tax Deductions: What You Can and Cannot Claim

2. Get Your Defence Allowances and Entitlements Right

Once your deductions are sorted, the next step is your allowances. How your ADF allowances are categorised can make a real difference to your return. Not all are treated the same way, and getting this right is worth the effort.

Deployment allowances vary in their tax treatment. Some may be fully taxable. Others, tied to overseas service in designated zones, may qualify for specific tax exemptions. It is worth checking the details for each type you receive.

The Rental Allowance (RA) you receive when you rent a private property does NOT form part of your assessable income.

The DHOAS subsidy itself is not assessable income. However, it is classified as a reportable fringe benefit, and a grossed-up amount may appear on your payment summary. This can affect income tests for payments related to Centrelink.

If you rent out the property linked to your DHOAS loan, the “otherwise deductible” rule may apply. This could mean the fringe benefit does not appear on your summary. A Defence-experienced tax professional can help navigate this area.

It is also worth checking how the Defence pay and conditions manual (PACMAN) categorises your allowances. Some may be split into taxable and non-taxable components, and getting this right on your return matters.

If you are unsure about a particular allowance, check the ATO’s ADF occupation guide. A specialist adviser familiar with Defence pay can also help clarify.

3. Use Strategies Beyond Deductions to Reduce Tax

With deductions and allowances covered, it is time to look at the bigger picture. Broader strategies can reduce your taxable income more meaningfully. These focus on how you structure your finances, not just what you claim.

Negative Gearing and Investment Property

Negative gearing occurs when the costs of holding an investment property exceed its rental income. The shortfall, which includes loan interest, maintenance, and management fees, can potentially reduce your overall taxable income. This may reduce your overall tax payable, depending on your situation

Here is a simple example. Say your ADF salary is $90,000, and your property runs at a $10,000 loss. In some cases, this loss may be applied against your income, which could reduce your taxable income and overall tax payable.

That said, negative gearing involves real out-of-pocket costs. The tax benefit does not remove the financial commitment of property ownership. Professional advice can help you decide if this approach suits your situation.

This is a simplified example for illustrative purposes only. Actual outcomes will vary depending on your individual circumstances and current tax rules.

Depreciation Schedules on Investment Properties

If you own a newer or recently renovated investment property, a depreciation schedule may unlock significant deductions. These are non-cash deductions based on the declining value of the building and its fixtures. This includes items like carpets, ovens, and air conditioning units.

A quantity surveyor prepares the schedule, and the deductions can run into thousands of dollars each year. This can be especially valuable in the early years of ownership. It can potentially turn a neutral property into one that also provides a tax benefit.

Salary Sacrifice into Superannuation

Salary sacrificing into super means directing pre-tax salary into your super account. These concessional contributions are taxed at 15% inside super. Your marginal tax rate is likely higher, so the gap can be meaningful.

The current concessional contributions cap is $30,000 per financial year. This includes your employer’s contributions. If you have not used your full cap previously, you may be able to carry forward unused amounts.

Unused amounts from up to five prior years may be available. This can be useful for those on higher ADF salaries or receiving deployment income. To claim these carry forward amounts, your total super balance must be below $500,000.

Rentvesting: The ADF Tax Advantage

Rentvesting means renting where you live while owning an investment property elsewhere. This can align well with the ADF lifestyle, especially during postings to new locations.

If you live in subsidised Defence housing, you can potentially keep your housing benefit while building a portfolio. Your tenanted investment property may allow you to claim rental deductions like loan interest, management fees, and depreciation.

This helps ADF members build long-term wealth without giving up housing entitlements.

Rentvesting also provides flexibility if you are unsure where to settle long-term. You build equity in one market while living where the ADF sends you. It suits the mobile nature of Defence careers.

4. Build a Property Investment Strategy

The strategies above work even better when combined with a property plan. For many ADF members, property investment can be a natural fit. Stable income, strong borrowing capacity, and Defence housing entitlements create a solid foundation.

When you are posted and living in subsidised housing, your living costs may be lower than civilian equivalents. This can free up cash flow to service an investment loan. The potential tax benefits of negative gearing and depreciation may further reduce your taxable income.

Frequent postings also suit a rentvesting model. You can live where the ADF needs you and invest where the numbers work.

Deductible costs on an investment property can include loan interest, council rates, management fees, insurance, and repairs. Capital works deductions may also apply, and any net rental loss can potentially offset your ADF salary.

Getting the ownership structure right matters too. Whether you purchase in your name, jointly, or through a trust affects how income and losses are distributed. It can also affect capital gains, so professional advice is valuable.

Spectrum has been helping Defence members build investment property portfolios for over four decades. Our approach connects your pay, entitlements, and property strategy into one integrated plan.

5. Explore Superannuation Strategies

Alongside property, super can be another powerful lever. Concessional contributions are taxed at just 15% inside super. For members on higher marginal tax rates, that gap can add up to meaningful savings.

Beyond salary sacrifice, there are additional strategies that may help your tax position. If your spouse earns less than $40,000 per year, you may be eligible for the spouse contribution tax offset. By contributing to their super, you could receive a tax offset of up to $540.

The government co-contribution may also be available if you earn under the income threshold and make after-tax contributions. The government can match 50 cents per dollar you contribute, up to $500 per year.

ADF members may have their super managed through CSC schemes such as MSBS, DFRDB, or ADF Super. Each fund has different rules and benefit structures. It is worth reviewing your scheme to see how voluntary contributions interact with your entitlements.

Unused concessional contributions may also be carried forward. This gives you flexibility to make larger contributions in years when you have more capacity to invest.

6. Get Your Record-Keeping and Timing Right

All of the strategies above rely on one thing: good records. Whether you are tracking ADF tax deductions or investment property expenses, solid record-keeping throughout the year makes tax time far less stressful. It also helps you claim everything you are entitled to.

Keep receipts and records of work-related expenses as you incur them. A dedicated digital folder or receipt-tracking app can save hours later. For phone or laundry claims, a four-week diary can form the basis of your annual calculation.

When lodging your tax return as an ADF member, timing matters. The ATO’s pre-fill service draws data from employers, banks, and government agencies. This data can take several weeks after the financial year ends to fully load.

Lodging too early may mean missing pre-filled information, which can lead to errors or omissions. Waiting a few weeks can help avoid these issues and give you a more complete return.

To reduce your taxable income for the current year, consider pre-paying deductible expenses before the financial year ends. This might include professional subscriptions, insurance premiums, or strata fees on an investment property.

7. Know When to Get Professional Help

Finally, knowing when to bring in a professional can tie everything together. For a straightforward return, self-lodging may be enough. However, if your situation includes investment properties or complex allowances, a specialist adviser can add real value.

A general tax agent can handle the basics. A Defence-specialist adviser understands ADF pay structures, DHOAS, HPAS, HPSEA, and deployment income. They can also help with posting-related property decisions.

The right adviser can connect your tax return to longer-term financial goals. This is where pay, property, and entitlements come together into a single plan, rather than being treated in isolation.

Tax agent fees are themselves tax-deductible. If professional help leads to more accurate claims, the cost can potentially pay for itself.

Want to see how your pay, entitlements, and property options connect? Book a free strategy session with Spectrum to explore what a Defence-specific plan could look like.

Frequently Asked Questions

Can ADF members claim gym memberships on tax?

Generally, no. Gym memberships are considered a personal expense by the ATO. An exception may apply if your role requires above-standard physical fitness, such as certain special forces positions.

Can I claim travel between home and base?

Your regular commute is considered private travel by the ATO. The exception is when you need to transport bulky equipment that cannot be stored at work.

Is the DHOAS subsidy taxable?

No. The DHOAS subsidy is not assessable income. It is reported as a fringe benefit, though, which may affect certain income-tested thresholds.

What is the difference between negative gearing and depreciation?

Negative gearing is when your property costs exceed rental income, creating a loss that may offset other income. Depreciation is a separate non-cash deduction for the decline in value of the building and its fixtures. Both can work together to reduce your taxable income.

Should I use a tax agent or do my own return?

If your situation is straightforward, self-lodging may work well. If you have investment properties or complex allowances, a tax agent experienced with Defence can be worth the cost. Their fee is also tax-deductible.

Disclaimer: This article provides general information only and does not constitute personal tax, financial, or legal advice. Tax rules can change, and individual circumstances vary. We recommend consulting a registered tax agent or qualified financial adviser for guidance specific to your situation.