27 Mar Mortgage Broker for Defence: How to Choose the Right Specialist

Finding the right mortgage broker Defence members can trust is more important than people often realise. ADF lending often involves income structures and service conditions that differ from standard civilian employment, and those differences can influence how lenders assess income and servicing. Choosing a broker who does not understand this environment can lead to costly mistakes.

It is important to note that not all brokers can offer DHOAS loans. These brokers can cost their clients hundreds of thousands of dollars because they offered a non-DHOAS loan solution without comparing against the benefits of a DHOAS loan. It is vital that you speak to a broker familiar with the DHOAS Scheme.

It is easy to assume all brokers assess ADF pay the same way. Allowance structures, posting cycles, deployment income and DHOAS integration can be misunderstood or assessed incorrectly. Borrowing capacity may be reduced, or the loan may be set up in a way that limits flexibility later.

Posting changes can happen quickly, so the loan structure needs flexibility for a move, a tenancy update, or an income mix change. Relocations across states, housing changes, and income adjustments can all affect a home loan. Strategy needs to account for Defence mobility, or members can end up stuck in a structure that does not support the next posting.

Deployment income adds further uncertainty. Some payments are linked to specific duties and timeframes, which can create confusion during assessment. A broker unfamiliar with Defence remuneration may either overlook income or rely on assumptions that do not hold up under lender scrutiny.

DHOAS brings another layer of complexity. Eligibility, approved lenders, and subsidy structures are governed by formal rules, and misunderstanding these requirements can affect long-term outcomes. Some members discover these details only after paperwork has begun.

The pressure point is clear. Defence careers are dynamic, yet many lending conversations are treated as static. This guide will help you decide whether you need a Defence specialist and how to choose the right one.

Why Defence Members Face Different Lending Rules

ADF income is structured differently from standard civilian employment. Lenders separate base salary from allowances and may treat each one differently during servicing. Broker choice can materially change the outcome of an application.

Base Salary vs Allowances

Base salary – Base salary is generally treated as stable, meaning it is usually counted more consistently in servicing.

Allowances – Field, sea, and deployment-related payments can be treated as variable, so lender policy can reduce how much is included and lower borrowing power.

Two banks can review the same ADF payslip and land on different results. A Defence mortgage broker members work with should know which lenders recognise specific allowances, plus the documentation each lender expects, since small policy differences can create large borrowing gaps.

Why Some Allowances Are Reduced or Excluded

Lenders assess risk by focusing on income consistency. If an allowance depends on role, location, or operational requirements, it may be treated as variable income. In those cases, the lender may apply shading or remove it from calculations entirely.

This can catch members off guard. A broker who understands Defence pay structures can explain how each income component is likely to be viewed. Clear guidance avoids unpleasant surprises mid-application.

Posting Cycles Change Loan Strategy

Posting cycles introduce mobility that the average borrower does not face. A property bought as a home may need to become an investment property after relocation. The loan structure needs to allow for that transition without unnecessary cost.

Product choice matters early. Features like splits, offset setup, and access to funds can influence flexibility later. A decision made today can create friction during the next posting.

A mortgage broker for ADF members should factor in relocation risk from the beginning. This includes selecting loan features that support flexibility if circumstances change. Planning early protects long-term options.

Deployment Income Inconsistencies

Deployment payments can lift total income for a defined period. Lenders often treat deployment-related income as variable, so the amount included can depend on how clearly it is shown across payslips and supporting documents.

A Defence loan specialist will know which lenders align best with Defence income profiles, and how to submit the documents so the assessment is clean. This can protect borrowing power and reduce delays once the application is in motion.

Interstate Purchasing Complexity

Some ADF members purchase property in a different state from where they are serving. Each state has its own duties, concessions, and legal requirements. Lenders may also apply location-based policy considerations.

A mortgage broker for Defence members should be comfortable managing interstate transactions. Coordinating lending, property location, and Defence movement requires experience. Proper structure ensures mobility does not create financial friction.

What a General Mortgage Broker Often Misses

Most brokers are skilled in standard residential lending. Defence lending involves additional policy layers that are easy to overlook without regular exposure to ADF scenarios. The difference between a general adviser and a mortgage broker that Defence members rely on often comes down to detail.

Misunderstanding DHOAS Eligibility

DHOAS operates under defined eligibility rules and approved lender panels. A broker unfamiliar with these requirements may assume the subsidy applies across all lenders, which is incorrect. A DHOAS mortgage broker should understand how entitlement tiers connect to specific loan products.

Common oversights include:

• Recommending a lender outside the approved panel

• Underestimating the value of DHOAS

• Failing to confirm the entitlement certificate timing

• Misunderstanding how refinancing or changing lenders may affect ongoing subsidy arrangements.

Small errors in this area can create delays or loss of benefit. Early clarity protects long-term outcomes.

Choosing Lenders That Ignore Key Allowances

Some lenders apply stricter policy settings to ADF allowances. A general adviser may default to a familiar bank without reviewing how field, sea, or operational payments are assessed. This can reduce borrowing capacity even when income history supports higher limits.

Typical policy gaps include:

• Shading variable allowances without review

• Excluding certain operational income types

• Applying more conservative servicing treatment than another lender may apply

A broker who understands Defence pay structures knows where lender policies differ. This knowledge directly affects serviceability assessment.

No Plan for Future Property Conversion

Relocation can turn a primary residence into an investment property. A loan structured purely for owner occupation may lack flexibility for that shift. Refinancing later can introduce avoidable costs.

A mortgage broker for ADF members should consider:

• Whether the loan supports future rental conversion

• How equity will be accessed

• What documentation will be required during the transition

Forward planning supports mobility. Without it, members may be forced into reactive changes.

Offset and Redraw Not Structured Strategically

Offset accounts and redraw facilities influence flexibility and cash flow control. If a property later generates rental income, the way funds were managed may have broader financial implications, so borrowers should obtain tax advice where required. Structure matters from day one.

Common configuration issues include:

• Mixing personal and future investment funds

• Linking accounts incorrectly

• Failing to explain long-term implications

A Defence loan specialist will structure these features deliberately. A clear setup avoids complications later.

Ignoring Posting Timelines

Loan selection should reflect likely career movement. Fixed terms, break costs, and portability options must align with expected relocation windows. Timing affects structure.

A mortgage broker for posted Defence members will factor in:

• Known posting cycles

• Potential interstate relocation

• Deployment-related timing risks

Professional guidance anticipates change rather than reacting to it. Strategic alignment reduces financial friction.

What a Defence Specialist Broker Does Differently

Clear differentiation comes from experience within the Defence environment. A mortgage broker Defence families rely on understands how military income, movement and entitlements interact with lender policy. The approach is structured around service conditions rather than a standard civilian template.

Understands ADF Pay Slips and Entitlements

An experienced ADF mortgage broker can read an ADF payslip beyond the headline salary figure. Each allowance category is identified, interpreted and presented in line with lender requirements. This ensures income is assessed accurately and documented correctly from the outset.

A broker who understands Defence pay recognises how entitlements vary by role and location. This insight reduces errors in serviceability assessment. Accurate income presentation can support a smoother assessment process.

Knows Which Lenders Count Deployment Income

Deployment-related payments require careful handling. Some lenders include these amounts under specific conditions, while others apply more restrictive treatment. A Defence mortgage broker Australia members engage will match the income profile to the lender policy.

Policy knowledge influences lender selection. Presenting deployment income clearly and appropriately improves assessment confidence. Appropriate lender selection may improve the way income is assessed.

Aligns Structure With Posting Cycles

Career mobility must shape loan structure. A mortgage broker for posted Defence members considers likely relocation windows before recommending product type or rate structure. Features are selected to support flexibility rather than restrict it.

This planning reduces exposure to break costs or unnecessary restructuring. The goal is continuity through movement, even when service circumstances change.

Integrates DHOAS Correctly

DHOAS involves approved lenders and defined eligibility criteria. A DHOAS mortgage broker ensures entitlement is confirmed and aligned with the chosen product. Integration is handled early to avoid disruption later.

Correct coordination supports long-term benefit. Misalignment can affect subsidy continuity. Careful execution preserves entitlement value.

Plans for Future Investment Conversion

Service movement can result in property role changes over time. A Defence home loan broker structures facilities to support a shift from owner occupation to rental use if required. This includes considering account configuration and funding strategy.

Forward planning strengthens flexibility. The structure anticipates change rather than reacting to it. Long-term options remain intact.

Handles Remote Approvals During Deployment

Operational commitments can limit availability for in-person processes. A military mortgage broker Australia members work with should be experienced in remote documentation and digital approval pathways. Clear communication ensures momentum continues despite location constraints.

Remote coordination requires organisation and lender familiarity. Efficient management reduces stress during operational periods. The process remains controlled.

Coordinates Lending With Broader Financial Strategy

Loan structure can interact with broader financial considerations, including tax and asset planning. Spectrum considers how lending decisions align with wider financial objectives. Coordination supports consistency across property and income strategy.

Coordination between lending strategy and a client’s broader financial and tax advice can help reduce gaps in decision-making. Each decision should support the same longer-term plan. Strategic alignment supports long-term financial stability.

If you would like to see how your allowances would be assessed, we can walk you through it in a quick clarity call.

How DHOAS Works With Your Home Loan

DHOAS is a home loan subsidy scheme for eligible current and former ADF members. Eligibility and entitlement depend on meeting the scheme’s service and other requirements, including qualifying service rules that apply from 1 July 2008. It is administered by the Department of Veterans’ Affairs on behalf of the Department of Defence.

What Is DHOAS

DHOAS provides a monthly subsidy that helps reduce home loan interest costs when scheme conditions are met, including occupancy requirements. To receive monthly payments, you need a DHOAS home loan with one of the Defence-nominated Home Loan Providers, and the subsidy is paid directly into the loan.

Eligibility Basics

Eligibility is based on completing a qualifying period of service and accruing service credit under the scheme rules. The official DHOAS guidance describes the qualifying service minimum as either consecutive Permanent service or effective Reserve service with minimum paid days per financial year.

In broad terms, the qualifying service minimum is described as:

• Permanent members – 2 years of consecutive service

• Reservists – 4 years of effective service, including 20 paid days per financial year

You also need a subsidy certificate, which is the proof of eligibility used to take out a DHOAS home loan. A subsidy certificate is required to take out a DHOAS home loan. Certificate status and timing should be confirmed before applying.

Tier Structure Overview

DHOAS uses service credit and tier levels, where longer service can increase entitlement and extend how long assistance can be received. Each tier has a subsidised loan limit that determines the portion of your home loan that can attract a subsidy.

How the Subsidy Integrates With Lender Choice

Defence has appointed a panel of three Home Loan Providers with the exclusive right to provide DHOAS home loans. The providers listed are:

• Australian Military Bank

• Defence Bank

• National Australia Bank

Your Home Loan Provider assesses your loan application using their own lending criteria, even if you are eligible for DHOAS. Comparing options still matters, since each of the three approved Home Loan Providers applies its own lending criteria and loan features.

Common Misconceptions

Several misunderstandings can affect decision-making:

• Believing DHOAS reduces as the the loan balance decreases

• Misunderstanding what drives DHOAS subsidy changes

• Assuming all banks can provide DHOAS loans

• Thinking that a subsidy certificate guarantees home loan approval

• Expecting unlimited subsidy beyond capped tier limits

• Assuming the subsidy can apply to more than one DHOAS home loan at a time

Should You Use a Defence Specialist?

By this point, the real question becomes practical. Do you need a standard adviser or a mortgage broker for Defence members? The answer often depends on how well your circumstances align with Defence-specific policy and movement.

A structured decision framework can remove uncertainty. Before choosing a Defence mortgage broker Australia members can rely on, ask:

1. Do they regularly work with ADF clients? Experience with service members builds familiarity with policy nuance and entitlement integration.

2. Can they clearly explain how your allowances are assessed?

A broker who understands Defence pay should outline how each income component is treated during a serviceability review.

3. Do they understand DHOAS lender restrictions? A DHOAS mortgage broker must know approved provider

requirements and how the subsidy interacts with the loan structure.

4. Have they structured loans around posting cycles before? Career movement should influence product selection and long-term flexibility.

5. Can they explain what happens if you convert to an investment? Owner-occupied to rental transitions require forward planning and clear structure.

If these questions cannot be answered confidently, it may indicate limited Defence exposure. Precision matters when policy layers are involved.

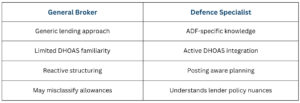

Below is a simplified comparison between a general adviser and a Defence loan specialist.

Choosing the right ADF mortgage broker influences more than approval speed. It affects flexibility, entitlement integration and long-term financial positioning.

Documents and Preparation Checklist

Preparation improves accuracy and speed. When engaging a mortgage broker for Defence members, having the right documents ready allows proper assessment from the beginning. Clear documentation reduces back and forth and strengthens lender confidence.

Below is a practical checklist used by a Defence mortgage broker:

• Service Record

This confirms the length and type of service, which can influence lender confidence and DHOAS eligibility discussions. It also provides context around career stability and progression.

• Two to Three Recent Payslips Showing Allowances

These should clearly display base salary and all relevant allowances. A broker who understands Defence pay will use these to map income correctly against lender policy.

• DHOAS Subsidy Certificate

If applying under the scheme, the current certificate should be provided. A DHOAS mortgage broker will confirm the validity period and ensure lender alignment before submission.

• Posting Orders, If Applicable

Current or upcoming posting documentation assists with planning. A mortgage broker for posted Defence members can factor relocation timing into the loan structure.

• Identification and Existing Loan Details

Standard identification is required for compliance. Details of any current loans help assess the overall position and future strategy.

Speak With a Defence Lending Specialist

Choosing the right mortgage broker Defence members rely on can influence flexibility, borrowing strength and long-term financial control. ADF careers involve movement, evolving income structures and entitlement rules that deserve careful alignment. Confidence comes from a clear strategy rather than guesswork.

A well-structured loan should support future relocation, protect subsidy eligibility and adapt as service conditions change. The right guidance brings certainty around income treatment, lender policy and long-term positioning. Strategic decisions today shape financial outcomes for years to come.

If you want clarity around your allowances, DHOAS position and posting outlook, speak with Spectrum. Request a Defence-focused lending review and see how your loan should be structured around your service career.

FAQs

Do I need a Defence specialist broker?

If your income includes multiple allowances, future relocation, or DHOAS integration, specialist experience can add clarity. A broker who understands Defence pay and policy alignment can reduce structuring errors. For straightforward scenarios, a general broker may suffice, though complexity increases the value of expertise.

Does it cost more to use a Defence mortgage broker that members trust?

No, broker remuneration is paid by the lender through commission. You should request a clear disclosure before proceeding.

Can I still use my bank?

Yes, you can approach your existing bank directly. However, your bank will assess you under its own internal policy without comparing other options. A Defence home loan broker can evaluate multiple lenders and determine which aligns best with your service profile.

Do all lenders accept DHOAS?

No. DHOAS only applies through approved Home Loan Providers listed on the official scheme website. A DHOAS mortgage broker should confirm lender eligibility before a formal application.

Can a broker help if I am posted interstate?

Yes. A mortgage broker for posted Defence members can coordinate lender requirements, property location considerations, and timing implications. Experience with interstate purchasing reduces avoidable friction.

Are there LMI waivers for Defence members?

LMI rules vary by lender and loan scenario. A broker can confirm current policy options for your deposit level, property type, and income profile before you apply. These are lender-specific rather than guaranteed benefits. A Defence loan specialist can clarify which institutions offer relevant options. Experienced brokers will also be aware of other avenues to avoid LMI such as Federal first home buyer incentive schemes, lender policy waivers or via the use of a Family Gurantee loan.

Can I rent out my home if I am posted?

Generally, yes, subject to lender approval and loan conditions. Conversion from owner occupation to rental may require notification or structural review. Early planning supports a smoother transition. Importantly, your DHOAS subsidy payments will continue unless you decide to remove DHOAS from your loan.

What happens to DHOAS if I refinance?

Refinancing may require a new subsidy certificate depending on the circumstances. DHOAS guidance explains that eligibility and certificate validity influence continuity of payments. Alignment with an approved provider remains essential. It is vital that you consider the effect on your DHOAS subsidy before refinancing.

Can a military mortgage broker assist members during deployment?

Yes. Remote documentation and digital approval pathways are common practice. A broker familiar with operational commitments can manage communication and lender requirements efficiently.