19 Nov How the Defence Home Ownership Assistance Scheme (DHOAS) Works in 2025

Australian Defence Force (ADF) members give years of service, yet many still find home ownership out of reach. Constant postings, confusing rules, and missed entitlements keep families renting for far longer than they need to. The Defence Home Ownership Assistance Scheme (DHOAS) was created to change that. It rewards service with real financial support.

In practice, DHOAS helps ADF members in two ways. Firstly, the additional funds received through DHOAS are included as income by the banks, which allows members to borrow more for their home.

Secondly, the DHOAS subsidy is literally money you receive to pay off your loan faster. An added benefit of these additional payments is the savings in interest on your home loan. The problem is that too many people don’t know how to use it properly, and end up missing out.

This guide shows the way through, with the latest 2025–26 updates, who’s eligible, how the tiers work, the steps to apply, and the key compliance points you need to know. If you want clarity on how DHOAS can work for you, this is where to begin.

Disclaimer: The information in this blog is general in nature and does not consider your personal circumstances, financial situation, or needs. It is not financial, taxation, or investment advice. You should seek independent professional advice before making any decisions.

What is DHOAS?

The Defence Home Ownership Assistance Scheme (DHOAS) exists to make housing more affordable for current and former ADF members. It provides a monthly subsidy on the interest of an approved home loan, rewarding service with direct financial support that helps families move from renting to ownership.

The scheme is established in Commonwealth legislation and administered by the Department of Veterans’ Affairs (DVA). On its website, DVA outlines the rules under The Defence Home Ownership Assistance Scheme, detailing eligibility, how service is counted, and the responsibilities that come with the benefit.

For ADF families, the impact is significant. DHOAS provides additional funds to pay off their home sooner and delivers a fair return for years of service. With the right guidance, it becomes a reliable tool for building stability and long-term financial security, rather than an entitlement that goes unused.

Who is Eligible for DHOAS?

Eligibility for the DHOAS is based on service time, type of service, and ongoing compliance with the scheme’s rules.

To qualify, members must meet the following:

- Minimum service requirements: Generally, four years of effective service before a first subsidy certificate can be issued.

- Permanent members: Entitlement accrues year by year while in full-time service.

- Reservists: Qualify through service credit, where part-time and interrupted commitments are converted into an equivalent period of full-time service.

- Breaks and combined service: Time across different branches or separated periods can often be added together.

- Post-separation eligibility: Former members can continue to access DHOAS for a set period, provided they meet occupancy requirements.

- Medical discharge: Members discharged for medical reasons may qualify immediately, even without the minimum service.

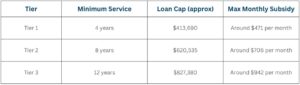

DHOAS Subsidy Tiers in 2025

Access to DHOAS is structured around three tiers, each tied to years of effective service, a loan cap, and a maximum subsidy amount. The longer the service, the greater the benefit available.

- Tier 1: Minimum 4 years of service. Provides entry-level access to the scheme.

- Tier 2: Minimum 8 years of service. Offers a higher loan cap and larger subsidy.

- Tier 3: Minimum 12 years of service. Delivers the maximum benefit available under DHOAS.

Subsidies are calculated against the ADF median interest rate, which is updated regularly to reflect market conditions.

The actual monthly payment depends on both the tier and the size of the approved loan, ensuring the support reflects real-world borrowing costs.

Comparison of DHOAS Tiers (2025)

Figures based on current 2025/26 rates. Subsidy is linked to the median interest rate and may vary.

We help members identify their tier and structure loans so every dollar of entitlement is put to work.

Common DHOAS Details Most Banks and Brokers Overlook

Most banks and brokers miss key DHOAS details that can significantly affect how much financial support ADF members actually receive.

- Subsidy payments are always based on the original loan balance, not the current loan balance. This means the benefit of DHOAS effectively increases over time, as it will cover more of the loan interest.

- Subject to the original loan balance and subsidy limits, members automatically receive a higher subsidy payment once their service qualifies for a higher tier.

- Not fully understanding how DHOAS works when obtaining a DHOAS loan can cost you tens of thousands of dollars over the life of the loan.

- There is also a lump sum payment option that allows some members to direct unused DHOAS subsidy credits towards reducing their loan balance upfront.

While the lump sum option has strict conditions, it can still be an effective way to cut debt in the right circumstances.

For example, an ADF member with six years of service can convert four years of DHOAS entitlement into a tax-free lump sum payment of $22,608. This amount is paid directly into the loan along with their first monthly DHOAS payment, enabling them to save interest on the reduced balance.

In most cases, these lump sum funds can also be accessed via redraw on the loan, providing a useful safety net of cash.

How to Apply for DHOAS

Accessing DHOAS involves a formal process that links your service record to an approved home loan and confirms you meet Defence occupancy rules.

1. Apply for a subsidy certificate via DVA. This certificate verifies your service record, confirms your tier, and sets the maximum loan amount eligible for subsidy.

2. Choose a DHOAS-approved lender. Only approved lenders can issue loans that qualify for the subsidy, and using a non-approved lender makes the benefit unusable.

3. Submit the subsidy authorisation form. This form connects your certificate to the mortgage, so the subsidy is paid directly to the loan each month.

4. Meet occupancy requirements. The property must be lived in for the minimum period outlined on DVA’s website, or the subsidy may be cancelled.

Latest Updates and Changes to DHOAS in 2025/26

The Defence Home Ownership Assistance Scheme is reviewed each financial year, and three key updates apply for 2025/26:

- Loan caps have been lifted

- Subsidy amounts have adjusted in line with interest rate changes.

- Compliance obligations are being reinforced by the Department of Veterans’ Affairs

Frequently Asked Questions

1. Can I continue to receive the subsidy if I rent out the property?

Yes, as long as you have completed the mandatory occupancy period, you will continue to receive DHOAS subsidy payments even if you move out and rent the property. However, you do have the option of cancelling the DHOAS payments at any time. Before doing so, we suggest obtaining advice, as you may not be able to restart DHOAS on that property in the future. In addition, if you are able to restart DHOAS, the payments may not be at the same level as previously received.

2. What happens if I refinance with a non-approved lender?

The subsidy stops immediately. To keep it active, refinancing must be done with a DHOAS-approved lender. It’s important to consider how refinancing to another DHOAS lender may affect your subsidy payments.

3. Do Reservists qualify under different rules?

Yes. Reservists use service credits that convert part-time service into full-time equivalents, which usually means it takes longer to qualify for each tier.

How Spectrum helps with DHOAS

First, we help you decide when to switch on DHOAS by modelling your service credits, tier, and posting cycle. This turns timing into a clear decision, not a guess. We compare activating the subsidy now versus waiting for a better window that fits your plans.

Next, we work out which lender serves you best. We assess all three DHOAS-approved lenders and compare borrowing capacity, rates, and product features side-by-side.

We make sure no entitlement goes to waste. Book your free consultation today and take full advantage of your DHOAS benefit.