10 Nov ADF Housing Benefits Explained: DHOAS, HPAS & HPSEA Guide 2025

Australian Defence Force (ADF) members are entitled to some of the most powerful housing benefits in Australia. These entitlements were designed to give service men and women a financial edge, helping them secure homes and build lasting stability.

The problem is that most people never unlock their full value. The rules are complicated, the timing can be confusing, and without clear guidance, thousands of dollars are often left on the table.

Many Defence families know these benefits exist, but are unsure how to use them to their advantage.

This guide changes that. With updated numbers, real case studies, and proven strategies, we explain how to maximise ADF entitlements and turn them into a genuine pathway to wealth.

Disclaimer: The information in this blog is general in nature and does not consider your personal circumstances, financial situation, or needs. It is not financial, taxation, or investment advice. You should seek independent professional advice before making any decisions.

Benefits of ADF Housing Entitlements

ADF housing benefits in Australia give members unique advantages that can ease costs and create a path toward long-term security. Yet many families never unlock their full value, and missed opportunities can mean tens of thousands of dollars lost.

These benefits work in different ways:

- Rental Allowance (RA): Subsidises private rent when service housing is unavailable, easing cash flow.

- Defence Housing Australia (DHA): Provides stable accommodation near bases, offering peace of mind.

- Living-in accommodation: Provides subsidised on-base housing close to duty locations, reducing day-to-day costs and commute time.

- Wealth-building entitlements: Programs like DHOAS, HPAS, and HPSEA provide significant monies to boost equity in your own home, turning support into lasting financial progress.

We bring together property, finance, and tax expertise to ensure no entitlement is wasted and every decision contributes to a stronger financial future.

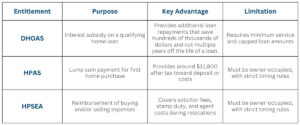

Defence Home Ownership Assistance Scheme (DHOAS)

The DHOAS is one of the most valuable ADF housing benefits Australia offers. It lowers the cost of owning a home by paying part of the interest on a qualifying loan.

Eligibility

- Permanent members qualify after two years of service.

- Reservists usually need four years of effective service

- Longer service unlocks higher subsidy tiers.

How it works

- The tax-free payment goes directly into your loan as an additional repayment each month.

- The amount depends on service length, capped loan limits, and interest rates.

- The DHOAS payments themselves can add up to hundreds of thousands of dollars over the life of the loan. These extra repayments, in turn, can save you hundreds of thousands in interest, allowing you to pay off your loan up to 10 years earlier.

Spectrum Financial Solutions has seen members use DHOAS to accelerate the repayment of their home loans to build equity faster. This dormant money in their home is then utilised towards building wealth.

With the right planning, this single entitlement can make the difference between just covering costs and moving ahead financially.

Home Purchase Assistance Scheme (HPAS)

The HPAS benefit provides a one-off payment to help Defence members buy their first home while serving in the ADF. The current amount is $16,949 before tax, which usually means around $11,800 after tax.

Home Purchase or Sale Expenses Allowance (HPSEA)

The HPSEA Defence scheme is designed to ease the cost of buying or selling a home when members are required to relocate for service.

Used wisely, it can prevent thousands of dollars in expenses from eroding savings during frequent moves.

What it covers

- Legal fees, such as solicitor or conveyancing costs.

- Stamp duty charges when purchasing a property.

- Agent fees are linked to selling an existing home.

How to use it strategically

- Plan the use of HPSEA during a posting cycle to absorb major costs.

- Free up savings that can then be redirected into deposits or loan reduction.

- Integrate with other ADF housing benefits in Australia to maximise entitlements across multiple moves.

Spectrum Financial Solutions guides members to apply HPSEA with intent, turning what is often seen as a reimbursement into a tool that supports a bigger financial plan.

When aligned with an ADF property investment strategy, this allowance helps families manage relocation costs while keeping momentum toward wealth building.

How the Entitlements Work Together

ADF housing benefits in Australia are most powerful when combined. Each scheme serves a different purpose, and when used together, they reduce costs, strengthen deposits, and make repayments easier to manage.

The impact grows further when these entitlements are paired with civilian incentives. First Home Owner Grants (FHOG), state stamp duty concessions, and even Lenders Mortgage Insurance waivers can all be layered on top of Defence housing subsidy programs.

This combination maximises ADF entitlements and reduces the financial pressure of getting into the market.

We have seen members combine HPAS with DHOAS and the FHOG. That single strategy lowered their deposit massively, reduced their repayments, and saved hundreds of thousands in costs.

Challenges and Critiques

Even with valuable housing support in place, Defence families face hurdles that can limit how much they benefit:

- Housing affordability outpacing benefits: Property prices have risen faster than the value of allowances, widening the gap between support and the real cost of home ownership.

- Payment timing delays: HPAS payments can be delayed, leaving members short of funds when they are most needed.

- Complexity without guidance: Strict rules and conditions make it easy to miss opportunities or reduce the value of entitlements.

- Relocation uncertainty: Frequent postings make planning for home ownership difficult, as members may hesitate to buy if unsure how long they will stay.

- Uneven awareness among members: Many know DHOAS or HPAS by name but lack clear information, leading to unclaimed benefits.

- Limited integration with civilian incentives: Grants, concessions, and LMI waivers can often be combined, but without advice, many miss out on these additional savings.

Strategic Tips to Maximise Your Benefits

Entitlements are most effective when they are applied with clear intent. These strategies help members turn support into lasting financial progress.

- Check service length and posting requirements before buying. Aligning purchases with eligibility dates ensures benefits are not lost.

- Direct subsidies toward properties with proven growth and rental demand. Avoid homes that fail to meet strong investment criteria.

- Live where service is required while investing where returns are stronger. This approach uses flexibility to accelerate wealth building.

- Stack benefits with FHOG, stamp duty concessions, or LMI waivers. The combined savings can amount to tens of thousands.

- Payments such as HPAS can be delayed. Always have a buffer to prevent cash flow stress at settlement.

- Longer service often unlocks higher tiers of support. Regularly reassessing eligibility ensures nothing is missed.

Defence housing benefits can fast-track home ownership and ease financial pressure, but only if used before the window closes. Too many families miss out on thousands in support through delays or a lack of guidance.

Spectrum Financial Solutions makes the process clear, combining property, finance, and tax expertise so every entitlement works for your future. Don’t leave wealth on the table, book your free Defence wealth strategy session today.

Check your eligibility for DHOAS by visiting www.dhoas.gov.au/

Disclaimer: The information in this blog is general in nature and does not consider your personal circumstances, financial situation, or needs. It is not financial, taxation, or investment advice.You should seek independent professional advice before making any decisions.